Section 8 - Distribution of Perkins Funding and Financial Requirements

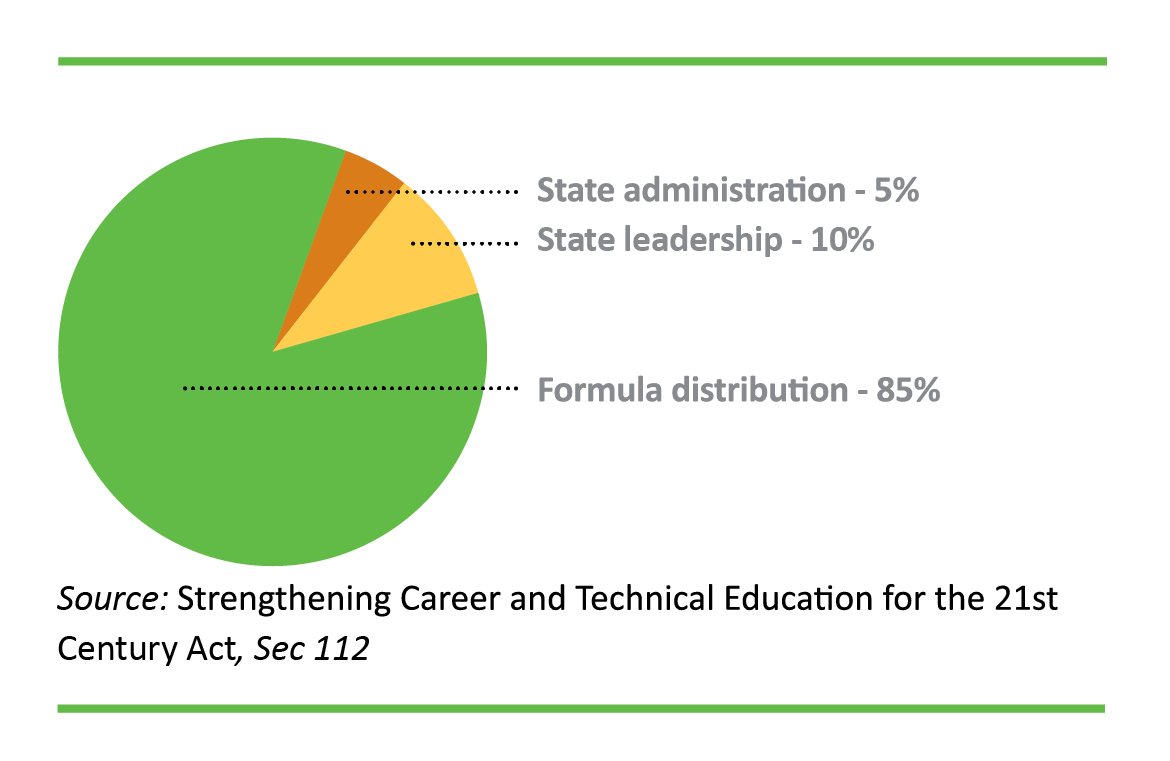

The purpose of this section is to offer transparency to the Perkins Federal Grant state allocation and the distribution of that allocation to the sub-recipients. As specified in the Act, Perkins V Title I funds allocated to the state are distributed among three categories:

- 85 percent – those provided to eligible recipients through formula-based distribution.

- 10 percent – those used for state leadership activities.

- 5 percent – those used for state-level administration of the grant.

The pie chart below reflects the distribution of Title One funds.

In the Minnesota 4-Year State Plan, sub-recipients are the local consortia that serve CTE programs at the secondary and postsecondary levels. These sub-recipients receive the 85 percent formula-based allocations.

The funds allocated to the formula-based distribution category are split between secondary- and postsecondary-eligible recipients as described in the state plan and illustrated in the chart <in figure 3 above>. All funds that are not used in the fiscal year awarded are recaptured and reallocated through the formula.

Distribution Formula

Eighty-five percent of the Perkins state allocation flows to Minnesota consortia by formula distribution. This 85 percent is further subdivided into the basic allocation (85 percent of the 85 percent) and the reserve (15 percent of the 85 percent). Under Perkins V law, states determine whether or not reserve funds are awarded and at what level up to a maximum of 15 percent. The distribution formulas are based on both the Perkins V Act (PDF) and the Minnesota 4-Year State Plan (PDF).

Calculations for the basic grant are based on specific attributes of the secondary and postsecondary constituents. While the dates of gathered data will change to utilize the most recent information, the basic formula remains constant.

Secondary Formula (Sec 131)The secondary formula is based on the most recent U.S. Census data for the population by school district of individuals aged 5-17 and also those aged 5-17 in households of poverty.

Thirty percent of the secondary allocation is based on the following:

- District population of individuals aged 5-17, compared to

- State population of individuals aged 5-17

Seventy percent of the secondary allocation is based on the following:

- District population of individuals aged 5-17 in poverty, compared to

- State population of individuals aged 5-17 in poverty

Results for each district are multiplied by the total secondary formula amount for Minnesota from the OCTAE allocation. The secondary consortium formula equals the sum of the amounts calculated for each district member in the consortium.

Postsecondary Formula (Sec 132)The postsecondary formula is based on the most recent number of postsecondary Pell Grant recipients. It compares:

- The number of Pell Grant recipients in the college, enrolled in Perkins-eligible programs, to

- The number of Pell Grant recipients in the state, enrolled in Perkins-eligible programs

Results for each college are multiplied by the total postsecondary formula amount for Minnesota from the OCTAE allocation.

The postsecondary consortium formula equals the sum of the amounts calculated for each college member of the consortium.

Under Perkins V, Section 112, reserve funds may be awarded to consortia in:

- Rural areas

- Areas with high percentages of CTE concentrators or CTE participants

- Areas with high number of CTE concentrators or CTE participants

- Areas with disparities or gaps in performance

Up to 15 percent of funds allocated to a consortium can consist of reserve funds. Reserve funds are unique in that they must specifically be used to either foster innovation or promote the development, implementation, and adoption of programs of study or career pathways aligned with high-skill, high-wage, or in-demand occupations. Innovation can be defined for this purpose as something not used before by a consortium or a new approach taken within a consortium. Consortia must describe in the grant application how reserve funds will be used. In Minnesota, fifteen percent of a consortium’s application will consist of reserve funds.

No more than 10 percent of the state’s allocation can be set aside to carry out state leadership activities. Of this amount:

- not more than two percent shall be dedicated to serve individuals in state correctional facilities,

- not less than $60,000, and not more than $150,000, shall be used for services that prepare individuals for nontraditional training and employment, and

- not less than the lesser of 0.1 percent or $50,000 shall be made available for the recruitment of special populations to enroll in CTE programs (Section 112(a)(2)).

Leadership funds are divided between secondary (42%) and postsecondary (58%) programs. Minnesota awards the majority of leadership funds to the Minnesota State System Office with the understanding that these funds serve statewide needs such as supporting the annual CTE Works! Summit, the mentorship program, and continuous improvement grants to consortia.

Leadership funds are intended to improve career and technical education including support for:

- Preparation for non-traditional fields, programs for special populations and other activities that expose students to high-skill, high-wage, and in-demand occupations;

- Individuals in state institutions including correctional and juvenile justice facilities and educational facilities serving individuals with disabilities;

- Recruiting, preparing, or retaining CTE teachers, faculty and support personnel; and

- Technical assistance for eligible recipients.

Additional annual leadership projects are awarded though a competitive process with a sponsor/supervisor at the state level.

The Perkins V Act, Section 112(a)(3), allows Minnesota to set aside no more than five percent of the state’s allocation or $250,000, whichever is greater, for administration of the state plan. These dollars are limited to the following uses:

- Developing the state plan

- Reviewing a local application

- Monitoring and evaluating program effectiveness

- Assuring compliance with all applicable federal laws

- Providing technical assistance

- Supporting and developing state data systems relevant to the provisions of the Perkins V Act;er

Dollars set aside for state administration must be matched on a dollar-for-dollar basis from non-federal sources.

Minnesota State Perkins V Finance Cost Centers

Minnesota State defines four parts to the finance process for college award recipients.

Federal requirements stipulate that each grant award activity deliver reports with the following attributes:

- Data consistency

- Report reproducibility

- Clear audit trail

- Ability to create consolidated annual reports

For each annual grant award, the System Office will assign unique general ledgers for the following categories with corresponding procedures: (NOTE: Colleges must use the general ledger (GL) provided by the System Office.)

Basic Grant – General Ledger (GL)

- The System Office grants accountant will assign a general ledger number for each new grant that should be used throughout the entire two-year grant period (Year two refers to reallocated dollars)

- A separate cost center must be set up for administration and a minimum of one other cost center must be established for the basic funds)

- Colleges must load the budgets per awarded amounts into ISRS (The total across all basic cost centers must equal the award)

- The local application must be approved by the Minnesota state director for career and technical education before any obligation of basic expenses

- Per the Perkins V Act, Minnesota State will recapture unused funds at the close of the state fiscal year (Around 15 of each year)

- The System Office grants accountant will assign a general ledger number for each new grant that should be used throughout the entire two-year grant period (Year two refers to reallocated dollars)

- A separate cost center must be set up for administration and a minimum of one other cost center must be set up in the reserve funds GL

- Colleges must load the budgets per awarded amounts into ISRS (The total across all reserve cost centers must equal the award)

- The local application must be approved by the Minnesota state director for career and technical education before any obligation of reserve expenses

- Per the Perkins V Act, Minnesota State will recapture unused funds at the close of the state fiscal year (Around 15 of each year)

- After the grant has been closed for the fiscal year, the Minnesota State System Office will recapture the unused basic and reserve funds from the postsecondary colleges (The recaptured funds are reallocated to local consortia according to a formula set forth by Perkins Local consortia are notified of the reallocated award no later than the end of February)

- The previous year’s basic grant GL will be reused for the reallocated basic grant GL, and the previous year’s reserve funds GL will be reused for the reallocated reserve funds GL

- A minimum of one cost center for each plan in the local consortium-approved application for the basic reallocation grant must be set up in the reallocated basic grant GL (In addition, at least one cost center per reserve reallocation plan must be set up in the reallocated reserve funds GL)

- Colleges must load the budgets per awarded amounts into ISRS (The total across all cost centers must equal the award)

- The local application must be approved by the Minnesota state director for career and technical education

- Per the Perkins V Act, unused reallocated funds cannot be reallocated to the consortium

- Intra-Agency Agreements: The System Office and colleges sign agreements for specific leadership projects

- Colleges incur expenses covered by the agreement

- After all (or partial, depending upon the agreement) expenses have been incurred, colleges generate an invoice(s) and send the invoice to the System Office (The receivable should be set up with the unique cost center that was established for the expenditures, with object revenue code 9806)

- Upon receiving the remittance from the System Office, colleges receipt the funds to the outstanding receivable, recording an off-setting revenue

- Leadership expenditures are not included with the standard draw (See Part 3 below)

- When a system college, as the primary employer, is engaged to provide services of its employees on a temporary basis to the System Office or another system institution, an approval letter or intra-agency agreement must be used

- An approval letter will be used if the assignment will result in a one-time payment of $500 or less

- Revised intra-agency agreement guidelines will be used if the assignment results in multiple payments or payment of $501 or greater

- It is essential that the parties at both institutions representing academic affairs, human resources, and finance be consulted prior to the execution of the agreement

- The process for reimbursement of expenditures by the contracting party to the service provision party should be clearly identified

- The home location will enter the assignment in the State College and University Personnel Payroll System (SCUPPS) with a category code created in SCUPPS to specifically identify FTE from another system This is essential for reporting purposes in Academic Affairs

- This process is intended to be used for hires between a campus and the System Office and, where applicable, between two campuses

Sub-grant agreements can be made from one college to another recipient college.

The recipient college (entity receiving grant funds from another college) records the actual grant expense and:

- Incurs permissible expenses and pays the expenditures from the applicable basic, reserve, reallocated basic, or reallocated reserve GL(s)

- Invoices the granting college for the incurred expenses. Invoice should be set up to distribute the receivable based on the expenditure’s cost center

- Uses payments from the granting college to grant revenue (Object code 9401)

The granting college (entity reimbursing another college) uses grant revenue as a pass through for both grant expenses and grant revenue to:

- Pay the invoice from the recipient college by debiting grant revenue (object code 9401) in the applicable Perkins GL(s) used by the recipient Do not use an expense object code

- The remittance amount (negative revenue) will be included in the next System Office draw The sub-grant portion of the funds received from the System Office should be receipted to grant revenue (object code 9401) to the applicable Perkins GL(s) associated with the invoice

- Grant revenue will have offsetting debit and credit entries

The Perkins V Act does not allow colleges or school districts to carry-over unexpended funds from one fiscal year to the next. All expenditure orders must be encumbered by June 30 of the local application fiscal year.

Attempts should be made to pay all invoices by June 30 of the local application fiscal year. Any payments to be made after July 30 must be cleared through the System Office grants accountant.

Basic grant, reserve funds, reallocated basic funds, and reallocated reserve funds will be reimbursed as follows:

- Set up cost center(s) with budget(s) totaling the award amount.

- System Office grants accountant reviews the Perkins cost centers associated with the current fiscal year for all colleges and determines the amount eligible for reimbursement.

- System Office grants accountant requests a drawdown from the Perkins fund maintained at the U.S. Department of Education to reimburse the colleges.

- System Office grants accountant enters a deposit into SWIFT for the drawn amount.

- System Office grants accountant sends an email to the fiscal contacts notifying them of the amount of the SWIFT deposit, and the specific amounts to receipt to which designated GLs.

- College fiscal contacts receipt the funds in ISRS to grant revenue (object code 9401), using Perkins cost center(s) associated with the designated GLs.

SERVS Financial System at MDE

Secondary programs are required to report expenditures using the Uniform Financial Accounting and Reporting System (UFARS) through the State Educational Record View and Submission (SERVS) financial system.

The SERVS financial system is a password-protected website for members of secondary educational organizations who have received prior approval to submit grant applications and create budgets, approve transactions, request fund reimbursement, or simply view grant applications and the budget management process.

Secondary fiscal agents will use the SERVS financial system to submit their Perkins applications, budgets, and expenditures. The fiscal agent will submit the consortium application and budget through the SERVS financial system website.

Once applications are approved, consortia will submit their expenditures through a drawdown request. Reimbursements will be made based upon the drawdown request.

All grant opportunities within MDE are found in the grants management directory of the SERVS financial system.